All Categories

Featured

Table of Contents

[/image][=video]

[/video]

If you're in excellent health and willing to undertake a medical examination, you may get approved for traditional life insurance at a much lower price. Surefire issue life insurance policy is typically unnecessary for those in great wellness and can pass a medical test. Because there's no medical underwriting, even those healthy pay the exact same premiums as those with health problems.

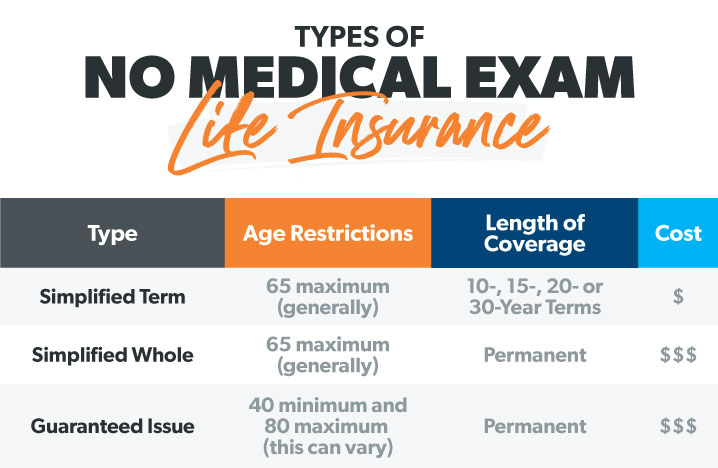

Given the lower protection amounts and higher costs, guaranteed problem life insurance may not be the most effective choice for long-term financial preparation. It's commonly much more suited for covering last costs as opposed to changing income or significant debts. Some guaranteed issue life insurance policy policies have age constraints, often limiting candidates to a details age variety, such as 50 to 80.

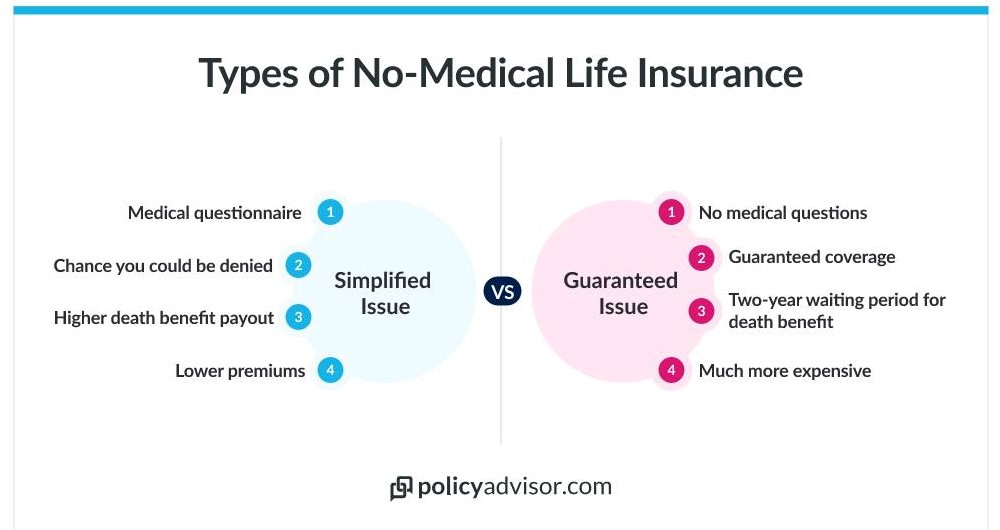

However, ensured problem life insurance policy features higher premium costs compared to clinically underwritten policies, yet prices can vary considerably relying on elements like:: Different insurer have different prices versions and may supply various rates.: Older candidates will pay greater premiums.: Ladies often have lower prices than men of the same age.

: The survivor benefit quantity impacts costs. A $25,000 policy costs less than a $50,000 policy.: Paying costs monthly costs extra general than quarterly or yearly payments.: Whole life premiums are higher overall than term life insurance plans. While the ensured concern does come at a cost, it supplies important protection to those that might not receive typically underwritten policies.

Guaranteed concern life insurance policy and streamlined issue life insurance policy are both sorts of life insurance policy that do not call for a medical examination. There are some critical distinctions in between the 2 types of policies. is a sort of life insurance that does not require any kind of wellness concerns to be addressed.

How Guaranteed Issue Life Insurance Policies can Save You Time, Stress, and Money.

However, guaranteed-issue life insurance policy policies typically have greater premiums and reduced fatality benefits than traditional life insurance policy plans. is a kind of life insurance coverage that does call for some health and wellness questions to be addressed. The wellness inquiries are generally much less extensive than those requested for typical life insurance policies. This indicates that simplified concern life insurance coverage policies might be offered to people with some health concerns.

Immediate life insurance protection is protection you can get a prompt answer on. Your plan will start as soon as your application is approved, indicating the entire process can be done in much less than half an hour.

First, immediate insurance coverage only relates to label plans with increased underwriting. Second, you'll need to be in excellent wellness to qualify. Many internet sites are encouraging split second coverage that begins today, yet that does not indicate every applicant will certify. Usually, customers will certainly send an application thinking it's for immediate insurance coverage, just to be met a message they need to take a medical examination.

The exact same information was then used to authorize or refute your application. When you use for a sped up life insurance coverage plan your information is examined quickly.

You'll then get instantaneous authorization, split second being rejected, or discover you require to take a clinical examination. You could require to take a medical examination if your application or the information pulled concerning you reveal any kind of wellness conditions or problems. There are numerous alternatives for instantaneous life insurance policy. It is very important to keep in mind that while numerous traditional life insurance policy companies deal increased underwriting with fast approval, you could need to go with an agent to use.

Little Known Facts About Life Insurance - Get A Free Quote Online.

The business listed below deal entirely on the internet, easy to use alternatives. They all offer the opportunity of an immediate decision. Ladder plans are backed by Fidelity Security Life. The company offers flexible, instant policies to individuals in between 18 and 60. Ladder policies allow you to make adjustments to your insurance coverage over the life of your policy if your requirements alter.

The firm uses policies to applications in between 21 and 55 for a ten-year term, and in between 21 and 45 for a 20-year term. You'll get an instantaneous decision from Bestow. There are no clinical exams needed for any type of applications. Principles plans are backed by Legal and General America. The firm doesn't provide plans to citizens of New york city state.

Just like Ladder, you may need to take a medical examination when you make an application for coverage with Ethos. The business claims that the bulk of candidates can get coverage without an examination. Unlike Ladder, your Ethos plan won't begin right now if you require an exam. You'll need to wait until your examination outcomes are back to get a rate and buy coverage.

In other instances, you'll need to provide even more info or take a clinical test. Here is a rate contrast of insant life insurance for a 50 year old male in good health.

Lots of people begin the life insurance policy buying policy by getting a quote. You can obtain quotes by getting in some standard details online like your age, gender, and general wellness standing. You can after that pick a company and change your strategy. Allow's state you got a quote for $50 a month for a $500,000, 20-year plan.

Higher benefit amounts and longer terms will certainly raise your life insurance policy prices, while lower benefit amounts and much shorter terms will certainly decrease them. You can set the specific coverage you're requesting and after that begin your application. A life insurance policy application will ask you for a great deal of details. You'll require to give your wellness background and your family members health history.

Cheap Life Insurance Without Medical Exams In 2025 (Top ... Fundamentals Explained

It is necessary to be 100% sincere on your application. If the firm locates you really did not divulge details, your policy might be denied. The decline can be mirrored in your insurance coverage rating, making it more challenging to get coverage in the future. When you send your application, the underwriting formula will analyze your information and pull information to come to an immediate choice.

A streamlined underwriting policy will ask you detailed concerns concerning your clinical history and current medical treatment during your application. An immediate problem plan will do the very same, yet with the difference in underwriting you can get an immediate decision.

Second, the insurance coverage amounts are lower, but the premiums are commonly greater. And also, assured concern plans aren't able to be utilized throughout the waiting duration. This means you can not access the full fatality advantage quantity for a set amount of time. For the majority of policies, the waiting duration is 2 years.

Yes. If you're in health and can qualify, an immediate issue plan will allow you to get coverage without examination and no waiting period. Suppose you remain in less than ideal health and want a policy without any waiting duration? Because instance, a streamlined concern plan without examination may be best for you.

Cheap Life Insurance Without Medical Exams In 2025 (Top ... Things To Know Before You Get This

Keep in mind that streamlined issue policies will take a few days, while instantaneous plans are, as the name suggests, split second. Acquiring an immediate plan can be a rapid and easy process, however there are a couple of things you should keep an eye out for. Before you strike that acquisition button make certain that: You're purchasing a term life plan and not an unintentional fatality policy.

They don't offer coverage for ailment. Some firms will issue you an accidental death plan immediately yet need you to take a test for a term life policy. You have actually reviewed the small print. Some websites are full of vivid pictures and bold guarantees. Make certain you read all the information.

Your agent has responded to all your questions. Just like sites, some representatives highlight they can get you covered today without explaining or offering you the details you need.

{kind=link}

Table of Contents

Latest Posts

An Unbiased View of Get Instant Life Insurance Quotes Online For Fast Coverage!

Some Ideas on Life Insurance: Policies, Information & Quotes You Should Know

The Greatest Guide To No Exam Life Insurance Quote - Nationwide

More

Latest Posts

An Unbiased View of Get Instant Life Insurance Quotes Online For Fast Coverage!

Some Ideas on Life Insurance: Policies, Information & Quotes You Should Know

The Greatest Guide To No Exam Life Insurance Quote - Nationwide